Problem on monopolistically competitive

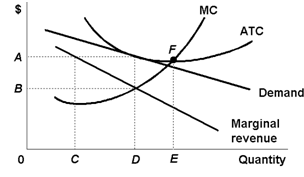

Refer to the given diagram for a monopolistically competitive firm give the answer of following question. Long-run equilibrium price will be: 1) above A. 2) EF. 3) A. 4) B.

When a household consumes just x and y, a higher price of y and the stable price of x will make: (i) All goods cheaper relative to the x. (ii) x cheaper relative to the y. (iii) Real family income grow. (iv) Substitution against x the more desirable. Q : Define the income elasticity of demand The income elasticity of demand is a measure of the: (w) relative responsiveness of quantity demanded to changes within income. (x) absolute change within demand yielded by an absolute change within income. (y) slope of the income-consumption curve. (

The income elasticity of demand is a measure of the: (w) relative responsiveness of quantity demanded to changes within income. (x) absolute change within demand yielded by an absolute change within income. (y) slope of the income-consumption curve. (

A city government trying to pass an excise tax for that the economic burden would be borne strictly through the seller will succeed when this imposes a tax on a good for that the price elasticity of: (i) demand is unitarily elastic. (

One of my friends can't find the answer of this question. Give answer of following economic based question. Tell me about strongly separable utility function?

geomeric method to measure elasticity of supply

Factor market: It comprises of factors of production namely land, labor, capital and associations.

When a demand curve is a negatively-sloped straight line, in that case demand is perfectly: (w) elastic where quantity demanded is zero. (x) elastic where price is zero. (y) inelastic where quantity demanded is zero. (z) elastic or inelastic all over

When physically and mentally capable individuals who are born in impoverished families fail to work after they develop up but since they can rely on charity, in that case they are experiencing: (1) involuntary poverty. (2) relative poverty. (3) a vicious cycle of pove

The resource most probable to be viewed as the fixed in short run by a firm which operates a cable TV and Internet connection system would be: (1) Unskilled workers who bury the cable. (2) The personal computer (3) Satellite dishes that it has leased to the customers.

Jana chugs 5 big cups of Gatorade in five minutes after winning the marathon. Jana’s marginal utility is much likely to be: (1) Equivalent for each cup as she was very thirsty. (2) Maximized at 3 cups, when she is reaching the equilibrium. (3) Diminishing whenev

18,76,764

1932191 Asked

3,689

Active Tutors

1440678

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!