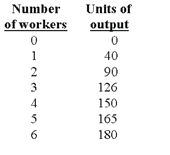

Problem on marginal returns

Select the right ans wer of the question. Refer to the following data. Diminishing marginal returns become evident with the addition of the: A) sixth worker B) fourth worker. C) third worker. D) second worker.

For a purely competitive market at any equilibrium point on the short-run supply curve: (w) all firms have identical marginal costs. (x) economic profit is positive. (y) accounting profit is normal. (z) marginal revenue = average cost. Q : Maximize output by monopolists Economists suppose that most monopolists wish for maximize: (i) accounting profit. (ii) the prices they charge. (iii) total revenue. (iv) economic profit. (v) output. I need a good answer on the topic of Ec

Economists suppose that most monopolists wish for maximize: (i) accounting profit. (ii) the prices they charge. (iii) total revenue. (iv) economic profit. (v) output. I need a good answer on the topic of Ec

A firm within an imperfectly competitive market is: (w) more likely to advertise than a purely competitive firm. (x) less probable to advertise than a purely competitive firm. (y) neither more nor less probable to advertise than a pure competitor. (z)

After Babble-On’s patents lapsed and entry and exit turned into possible in this illustrated figure of market, in the long run Babble-On would be expected to: (i) continue to reap economic profits. (ii) break even and experience zero economic pr

As the price falls by P4 to P3 to P2 to P1 beside such demand curve for Pixie's cheesy fried grits, then total revenue: (w) always rises. (x) always falls. (y) rises then falls. (z) falls then rises. Q : Opportunity Cost to the User An An opportunity cost to the user, although not to society as an entire, which would be the: (w) accounting profits realized by a firm of CPAs. (x) interest paid by a borrower for a bank loan. (y) rent paid by a sharecropper to a plantation owner. (z) m

An opportunity cost to the user, although not to society as an entire, which would be the: (w) accounting profits realized by a firm of CPAs. (x) interest paid by a borrower for a bank loan. (y) rent paid by a sharecropper to a plantation owner. (z) m

In an economy the MPC is 0.75. Investment expenses in the economy raise by Rs.75 crore. Compute total increase in national income.

Cartels are generally supported most strongly by: (w) the largest and most efficient producers in the industry. (x) the weakest and least efficient producers in the industry. (y) buyers of the output of the industry. (z) consumer advocate groups.

Contestable markets and purely competitive markets share the feature of: (w) collusive behavior of huge firms. (x) freedom of entry and exit into the long run. (y) widespread product differentiation. (z) persistent economic profits. Q : Right-to-Work Laws I have a problem in I have a problem in economics on Right-to-Work Laws. Please help me in the following question. The supporters of unions might complain that right to work laws frequently permit non-union workers to: (i) ‘Free-ride’ by enjoying the union-negotiated advantag

I have a problem in economics on Right-to-Work Laws. Please help me in the following question. The supporters of unions might complain that right to work laws frequently permit non-union workers to: (i) ‘Free-ride’ by enjoying the union-negotiated advantag

18,76,764

1933730 Asked

3,689

Active Tutors

1457382

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!