Problem on equilibrium price

Refer to the following data. Equilibrium price will be: A) $4. B) $3. C) $2. D) $1. Give the answer of above questaion

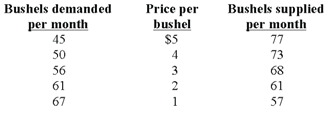

Refer to the following data. Equilibrium price will be: A) $4. B) $3. C) $2. D) $1.

Give the answer of above questaion

Opponents of the current welfare system who desire the welfare system scaled down tend to argue which this: (1) has constantly experienced funding cuts for the past decade. (2) cannot succeed in helping poor people within a market economy. (3) stimula

Assume that a firm with the market power in output market wishes to grow and that hiring more workers needs it to increase salaries 8 percent for all the workers. The output prices will most likely: (i) Increase 8 percent to cover the wage rise. (ii) Increase less tha

The kinked demand curve model of oligopolistic pricing behavior reflects the concept which: (1) price hikes fail to accommodate small hikes in costs. (2) other firms ignore price hikes by single firms. (3) other firms match any price cuts by any singl

Can someone please help me in finding out the accurate answer from the following question. Labor contracts having agency shop arrangements need: (1) Employees of a firm to give dues to the union. (2) The firm to hire just union members. (3) New employees of the firm t

A surplus of papayas would involve when: (1) government set a price ceiling of P1. (2) growers expected prices to soar. (3) hurricanes vanished all Central American papaya plantations. (4) government imposed a price floor of P2. (5) seller's supp

The non-discriminating organization with monopsony power in the labor market confronts the: (i) Wage rate which consistently surpasses the marginal revenue. (ii) MRP less than w. (iii) MFC which surpasses w. (iv) Monopolistic seller of the organization’s output.

In illustrated graph below, supply is mostly perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c. (iv) point d. Q : Procedure of substituting complicated The procedure of substituting complicated machinery for human labor is termed as: (1) automation. (2) bionic engineering. (3) scientific management. (4) robotics. (5) industrial sabotage. How can I solve my

The procedure of substituting complicated machinery for human labor is termed as: (1) automation. (2) bionic engineering. (3) scientific management. (4) robotics. (5) industrial sabotage. How can I solve my

When the price reduces and quantity demanded increases along such demand curve for pizza, in that case the slope: (w) is constant and elasticity falls. (x) and elasticity are constant. (y) increases and elasticity is constant. (z) and elasticity increase.

Suppose that all these demonstrated curves are infinitely long straight lines. So, a supply curve for that price elasticity of supply is constant for each possible price and quantity is: (i) supply curve S2. (ii) supply curve S3. (iii) supply curve S5

18,76,764

1948889 Asked

3,689

Active Tutors

1443542

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!