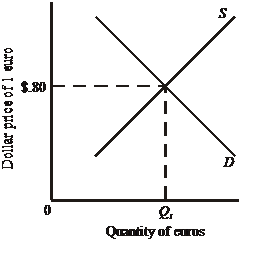

Give me answer of this question. Refer to the following diagram. Other things equal, a rightward shift of the demand curve would: A) depreciate the dollar. B) appreciate the dollar. C) reduce the equilibrium quantity of euros. D) depreciate the euro.