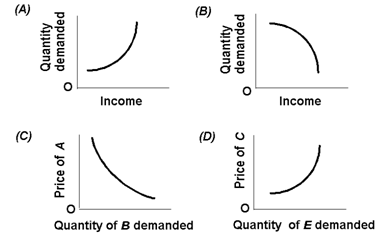

Problem on coefficient of income elasticity

Refer to the following diagrams give the answer of following question. In which case would the coefficient of income elasticity be positive? 1) A 2) B 3) C 4) D

Since of the high probability of bankruptcy and default of a latest corporation, new corporations: (i) Encompass little trouble selling bonds. (ii) Would prefer to the issue stock. (iii) Encompass more trouble selling bonds than the established corporations. (iv) Woul

Subsequent to Judith buys an American eagle shirt at the mall for 50 percent off, she purchases the matching purse, skirt and earrings. Such extra purchases are illustrations of: (i) Complementary goods. (ii) Substitute goods. (iii) Numbers and ages of the buyers. (iv

Why the coefficient of price elasticity of demand is is negative?

Lower bond prices arise simultaneously while there are increases into: (1) optimism among investors in economic capital. (2) government budget surpluses. (3) the rates of saving by households. (4) the liquidity of all financial assets. (5) interest ra

Within the long run, a monopoly cannot continually produce economic profit unless: (w) economies of scale are important. (x) corporate taxes are lowered. (y) barriers to entry are significant. (z) the monopolist maximizes profit.

Siberian Software vends custom programs to the multinational corporations. Its programs are coded in a remote region. In equilibrium, the Siberian’s programmers produce a marginal revenue product equivalent to around: (i) $21 per hour. (ii) $25 per hour. (iii) $

Can someone please help me in finding out the accurate answer from the following question. The pure monopsonist: (1) Is the sole buyer of a specific good or resource in the given market. (2) Can adjust just quantity and therefore is a price-taker in input market. (3)

Hey friends I need your help for illustrates that this is NOT true by monopolies: (1) are generally more profitable in the long run when there are barriers to entry. (2) sometimes incur losses. (3) may try to increase demand by marketing. (4) shut down while faced by

Consumers’ demand prices and sellers’ supply prices may be different in equilibrium due to: (w) arbitrage. (x) expectations about availability. (y) the invisible hand. (z) government subsidies or tax wedges.

In the short run, no profit-oriented monopolistically-competitive firm still knowingly generates any output unless: (1) an economic profit is assured. (2) total revenues are expected to equal or exceed its total variable costs. (3) the average wage ra

18,76,764

1922236 Asked

3,689

Active Tutors

1432880

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!