Problem based on shift of the production possibilities curve

Technological advance in producing both capital goods and consumer goods is illustrated by the shift of the production possibilities curve from AB to: 1) CD. 2) EB. 3) AF. 4) GH. Select the right answer for above given question

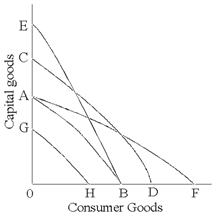

Technological advance in producing both capital goods and consumer goods is illustrated by the shift of the production possibilities curve from AB to: 1) CD. 2) EB. 3) AF. 4) GH.

Select the right answer for above given question

The Christmas tree industry’s short-run supply is demonstrated as: (1) curve A. (2) curve B. (3) curve E. (4) curve F. (5) curve G. Q : Price leadership models When all firms When all firms in an oligopolistic industry raise and lower prices together, in that case it is most consistent along with: (w) the kinked demand curve. (x) price leadership models. (y) the herd instincts of investors. (z) competitive theories of cart

When all firms in an oligopolistic industry raise and lower prices together, in that case it is most consistent along with: (w) the kinked demand curve. (x) price leadership models. (y) the herd instincts of investors. (z) competitive theories of cart

Can someone please help me in finding out the accurate answer from the following question. Employer with the monopsony power which as well had the ability to wage discriminate perfectly would tackle a marginal factor cost of labor

I have a problem in economics on spending pattern in Substitution Effects. Please help me in the following question. Even when your real income were held steady by adjusting for price modifications, your spending pattern would react to modifications in relative prices

The firm’s net revenue grows whenever the price of a good is cut when the price elasticity of: (i) Demand surpass the price elasticity of supply. (ii) Replacement goods are less than one. (iii) Supply is in an associatively elastic range. (iv) D

The most important declines in opportunity costs of multiple goods for the consumers and greatest rises in the value of net production for all societies everywhere tend to be realized whenever production is organized in accord by: (1) The optimal clas

Financial assets will create lower rates of return to prospective investors while: (w) they become more liquid. (x) their prices go up. (y) interest rates increase. (z) default risks decrease. Hey

Can someone help me in finding out the right answer from the given options. The employer who amplifies the safety of a place or prospects for advancement to the job applicants makes inefficiencies (or arguable inequities) since of: (1) Signaling. (2) Credentialism. (3

For this profit-maximizing brickyard the total revenue equals approximately: (i) $600 per day. (ii) $900 per day. (iii) $1200 per day. (iv) $1530 per day. Q : Demand for loanable funds An increase An increase in the demand for loanable funds is reflected within an increase in the: (1) term structure of interest rates. (2) demand for money. (3) supply of bonds. (4) supply of money. (5) demand for bonds. I nee

An increase in the demand for loanable funds is reflected within an increase in the: (1) term structure of interest rates. (2) demand for money. (3) supply of bonds. (4) supply of money. (5) demand for bonds. I nee

18,76,764

1946493 Asked

3,689

Active Tutors

1460597

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!