Problem based on ATC-MR and MC

If $4 is Firm B's profit-maximizing price, its: A) ATC must be $4. B) MC must be $4. C) MR must be $4. D) MC must be zero. Help me to get through this problem.

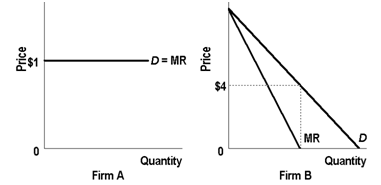

If $4 is Firm B's profit-maximizing price, its: A) ATC must be $4. B) MC must be $4. C) MR must be $4. D) MC must be zero.

Help me to get through this problem.

When this firm is typical into this purely-competitive of constant-cost industry, as in demonstrated figure in long-run equilibrium for cranberries will be attained at a market price of: (i) P1. (ii) P2. (iii) P<

When market demands for agricultural products are relatively price inelastic and relatively income inelastic both, in that case as per capita income raises, the average income of farmers will: (w) increase while supplies of agricultur

Maximum possible total revenue monthly from sales of RoboMaids is about: (i) $70 million. (ii) $100 million. (iii) $125 million. (iv) $170 million. (v) $230 million. Q : Labor Unions and Employment job The labor union will not get better its member’s job prospects through: (i) Raising the worker productivity through apprenticeship. (ii) Restricting entry through quotas or high initiation fees. (iii) Lobbying for the tariffs on competing foreign goods. (iv) Col

The labor union will not get better its member’s job prospects through: (i) Raising the worker productivity through apprenticeship. (ii) Restricting entry through quotas or high initiation fees. (iii) Lobbying for the tariffs on competing foreign goods. (iv) Col

Can someone please help me in finding out the accurate answer from the following question. Practices that were common in the labor markets however that are now illegal comprise: (i) Boycotting, scabbing and shirking. (ii) Sweetheart deals assembly line speedups and st

When the price falls along such demand curve for pizza, in that case total revenue: (w) falls. (x) rises, then falls. (y) rises. (z) does not change. Q : Price below perfect competition Who Who decides price beneath perfect competition? Answer: Price under perfect competition is recognized by the forces of market demand and supply in business.

Who decides price beneath perfect competition? Answer: Price under perfect competition is recognized by the forces of market demand and supply in business.

When Serena Williams, Cindy Crawford, Hillary Clinton, Katy Couric, Jennifer Lopez, and Ashanti all start wearing Wal-Mart jeans at public appearances, economists would explain any resultant raise in Wal-Mart’s jean sales to the change in: (1) Expectations regar

Buying since you expect a price to increase, at that point you will sell, which is termed as: (w) arbitration. (x) speculation. (y) profiteering. (z) arbitrage. Hey friends please give your opinion for the problem

Can someone help me in finding out the right answer from the given options. In the year 1950 the federal government enhanced interstate highways, therefore decreasing the: (1) Demand for and the volume of highway travel. (2) Growth rate of city sprawl. (3) Demand for

18,76,764

1947527 Asked

3,689

Active Tutors

1425465

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!