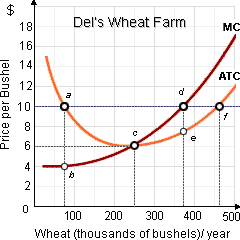

When the world price for this year’s wheat crop is $10 per bushel, and Del, a profit maximizer one who owns the biggest wheat farm within North Dakota: (i) is a quantity taker and a price adjuster. (ii) cannot generate an economic profit into the short run. (iii) is a price taker and a quantity adjuster. (iv) produces at point c, here average total cost is minimized. (v) realizes $4 per bushel into excess profits.

Hello guys I want your advice. Please recommend some views for above Economics problems.