Price inelasticity of supply

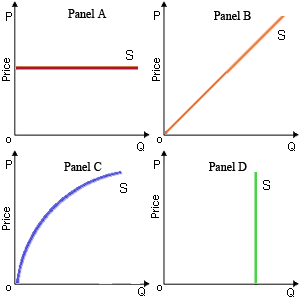

The price elasticity of supply is zero therefore supply is perfectly price inelastic within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Can someone explain/help me with best solution about problem of Economic...

The price elasticity of supply is zero therefore supply is perfectly price inelastic within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Can someone explain/help me with best solution about problem of Economic...

Oligopolies which unite to form cartels and share monopoly profits give an illustration of: (i) collusive behavior. (ii) territorial imperatives. (iii) mergers and acquisitions. (iv) non-collusive strategy. (v) corporate raiding.

Of the given price elasticities [ed] for market demand curves, there the one which is absolutely implausible by the vantage of standard economic theory would be one for that, across all conceivable ranges of prices: (1) ed= 0 and the

Price discrimination in the sale of a good show charging various prices that: (w) reflect differences in production costs. (x) do not reflect differences in production costs. (y) are dictated by market conditions. (z) cause a monopoly to be inefficien

The typical firm produces in a purely-competitive long-run equilibrium where price equals as: (1) short-run average cost. (2) marginal cost. (3) long-run average cost. (4) average revenue per unit. (5) All of the above. Q : Can GDP be more than GNP Can GDP be Can GDP be more than GNP? Answer: Yes, GDP can be greater or more than GNP if NFIA is negative.

Can GDP be more than GNP? Answer: Yes, GDP can be greater or more than GNP if NFIA is negative.

Define the term Psychological Pricing and what are their aspects?

When a 2% raise in the price of Kibbles causes a 1% raise in the quantity sold of Bits, in that case their price cross elasticity of demand is approximately _____ and such goods are _____. (w) -2; complements (x) 0.5; substitutes (y) 2; substitutes (z

I have a problem in economics on Stockholders of a big business corporation. Please help me in the following question. The stockholders of a big business corporation: (1) Frequently manage the everyday output decisions. (2) Usually own big percentages of the total sha

A monopoly might emerge naturally while economies of scale: (w) are small relative to market demand. (x) do not exist. (y) are large relative to market demand for output. (z) and average costs are rising over the market output range. Q : Price inelastic over relevant range of When the market demand for wheat is price inelastic over relevant range of prices, fluctuations within the supply of wheat will cause incomes of wheat farmers to: (w) increase when supply decreases and decline while the supply of whea

When the market demand for wheat is price inelastic over relevant range of prices, fluctuations within the supply of wheat will cause incomes of wheat farmers to: (w) increase when supply decreases and decline while the supply of whea

18,76,764

1928581 Asked

3,689

Active Tutors

1431013

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!