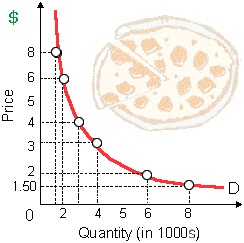

Since the price drops/falls from $8 to 1 all along this demand curve, the price elasticity of demand for pizza: (1) increases towards infinity. (2) Drops/Falls towards zero. (3) Increases, then drop/falls. (4) Always equivalents 1 and demand is unitarily elastic.

Can someone help me in getting through this problem.