Price elasticity of demand DVDs of games

Moving from point c to point d beside demand curve D, the price elasticity of demand DVDs of video games equals: (1) 0.8. (2) one. (3) 1.10. (4) 1.25. (5) 2.50 Can someone explain/help me with best solution about problem of Economics...

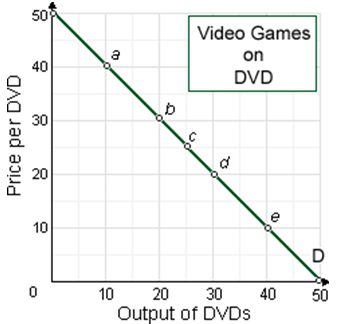

Moving from point c to point d beside demand curve D, the price elasticity of demand DVDs of video games equals: (1) 0.8. (2) one. (3) 1.10. (4) 1.25. (5) 2.50

Can someone explain/help me with best solution about problem of Economics...

The contribution standard of income distribution: (w) sets the least efficient incentives for production. (x) is the distribution standard most compatible along with pure capitalism. (y) minimizes individual economic freedom. (z) is very complimented

Labor productivity tends to rise while: (1) the K/L ratio increases. (2) the K/L ratio decreases. (3) workers forego education. (4) capital becomes more expensive. (5) wage levels fall. Please choose the right answ

is the price in the law of demand an absolute price or a relative price

Price cross elasticity of demand measures the responsiveness of: (1) quantity of a good sold to changes within its price. (2) quantity sold to changes within income. (3) price of one good to changes within the sales of other. (4) amount demanded of on

The substitution effect signifies to the change in consumption pattern as: (1) The absolute price of the good modifications. (2) Income changes. (3) The relative price of good changes. (4) The quality of good changes. Can someone p

The firm’s net revenue grows whenever the price of a good is cut when the price elasticity of: (i) Demand surpass the price elasticity of supply. (ii) Replacement goods are less than one. (iii) Supply is in an associatively elastic range. (iv) D

Short-run supply curve of a purely competitive firm’s is the positively sloped part of the marginal cost curve which is above its: (w) average fixed cost curve. (x) resource demand curve. (y) average variable cost. (z) short-run

When a purely competitive industry is within equilibrium as well as all firms in the industry are operating along with economies of scale, in that case the industry is in: (w) long-run and short-run equilibrium. (x) short-run equilibrium and long run

Within a competitive industry into the long run: (w) economic profits are common. (x) existing firms wither in growing industries. (y) economic profits induce new firms to enter an industry. (z) accounting profits will be zero for all firms.

Money: Money is what money does. Or Money is something that is accepted as a medium of exchange and at similar time act as a store of value.

18,76,764

1939462 Asked

3,689

Active Tutors

1455435

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!