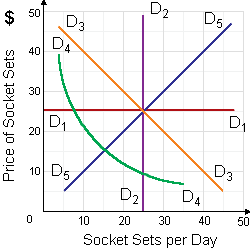

In this demonstrated figure, there the price elasticity of demand coefficient is: (1) one at the midpoint. (2) greater than one in range a. (3) less than one in range b. (4) falling along with movements down along the demand curve. (5) All of the above.

How can I solve my Economics problem? Please suggest me the correct answer.