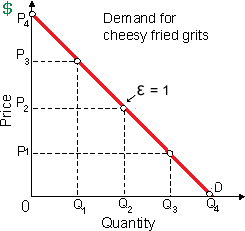

Moving by left to right along demand curve D, then price elasticity of demand for cheesy fried grits of Pixie is mostly: (w) positive, then unitary, then negative. (x) constant and equivalent to one. (y) greater at high prices than at low prices. (z) lower at high prices than at low prices.

Hello guys I want your advice. Please recommend some views for above Economics problems.