Price elasticity of demand among various prices

The price elasticity of demand as in below illustrated figure for DVD games among prices of $20 and $30 is about: (w) 1.00. (x) 25. (y) 1/25. (z) 1/2. Please choose the right answer from above...I want your suggestion for the same.

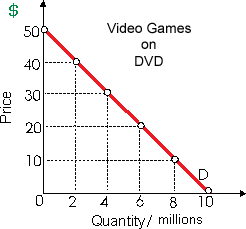

The price elasticity of demand as in below illustrated figure for DVD games among prices of $20 and $30 is about: (w) 1.00. (x) 25. (y) 1/25. (z) 1/2.

Please choose the right answer from above...I want your suggestion for the same.

I have a problem in economics on Equilibrium for a price maker firm. Please help me in the following question. In equilibrium, for a price maker firm, the charge of monopolistic exploitation is any difference among: (1) P and MR. (2) P and MC. (3) VMP

Production function: It is the technological relationship among input and output of a firm and is termed as production function.

Nostalgia Corporation could accomplish minimum average costs for Silver Screen DVDs when this produced: (i) 4 million DVDs. (ii) 6 million DVDs. (iii) 8 million DVDs. (iv) 10 million DVDs. (v) 12 million DVDs.

Can someone please help me in finding out the accurate answer from the following question. The outcomes of strikes do not comprise: (i) Losses of the perishable products. (ii) Shipping delays. (iii) Decreased production costs. (iv) Shortages.

When the annual interest rate is 12 percent and a rental house can be expected to rent perpetually for price of $1,000 monthly, in that case the house has a present value of approximately: (1) $240,000. (2) $144,000. (3) $100,000. (4) $72,000. (5) $12

Tell me the answer of this question. Economists would describe the U.S. automobile industry as: A) purely competitive. B) an oligopoly. C) monopolistically competitive. D) a pure monopoly.

An illustration of rational ignorance is demonstrated when you: (1) Are elected to a political office. (2) Settle for an other half who is not your "ideal" mate. (3) Eat a steak which increases your cholesterol level. (4) Were suspended from high scho

Balance of trade: It is the distinction between imports and exports of a country which are valued.

The yellow dog contracts are now proscribed, however in the early 20th century such agreements among employers: (i) Not to purchase intermediate goods made by unionized labor hindered labor market transformations. (ii) And workers stating that the workers would not jo

When a purely competitive industry is into long-run equilibrium: (i) firms try to maximize profit. (ii) P = ATC. (c) P = MC. (iii) economic profit is zero. (iv) All of the above. Can someone explai

18,76,764

1950996 Asked

3,689

Active Tutors

1418538

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!