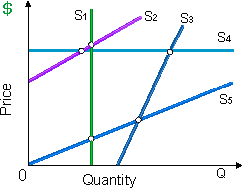

Suppose that all these curves are infinitely long straight lines. There supply curve which is relatively (although not perfectly) price elastic for all quantities and prices is: (1) supply curve S1. (2) supply curve S2. (3) supply curve S3. (4) supply curve S4. (5) supply curve S5.

Hey friends please give your opinion for the problem of Economics that is given above.