Precise Equality of Income Distribution

Precise equality of income distribution is demonstrated by: (1) line 0A0'. (2) line 0B0'. (3) line 0C0'. (4) line 0D0'. (5) line 0E0'. Can someone explain/help me with best solution about problem of Economics...

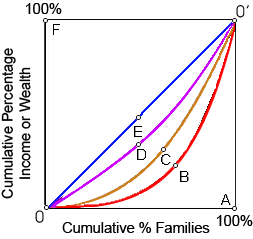

Precise equality of income distribution is demonstrated by: (1) line 0A0'. (2) line 0B0'. (3) line 0C0'. (4) line 0D0'. (5) line 0E0'.

Can someone explain/help me with best solution about problem of Economics...

Give me answer of this question. Which of the following arguments comes closest to constituting a legitimate economic exception to the case for free trade? A) the increase-domestic-employment argument B) the cheap-foreign-labor argument C) the diversification-for-st

I don't know how to do this kind of homework

When the resource market shown in this illustrated figure is initially within equilibrium along with demand curve D0: (w) owners of these resources currently receive no economic rents. (x) economic rent is specified by area

When D0 is the initial demand curve for land in this illustrated figure, within equilibrium the economic rent realized through the landowner will be: (1) zero. (2) area Ocef. (3) area cae. (4) area Oaef. (5) a pure economic

A firm’s perception which competitors will match price cuts but avoid price hikes yields: (w) price leadership behavior. (x) limit pricing structures. (y) kinked demand curves. (z) monopolistic competition. Can anybody sugges

The production possibilities frontier graphically demonstrates the: (i) Production limitations which confront the society. (ii) Benefits inherent in the capitalistic economy. (iii) Social selections available if technology is boundless. (iv) Structura

The most complementary of the given pairs of goods are: (1) organic vegetables and French fries. (2) polyester fabrics and cotton cloth. (3) transistor radios and televisions. (4) jogging shoes and bicycles. (5) pencils and erasers. Q : Profit from predatory pricing In order In order for a firm to profit from predatory pricing: (w) the incumbent must fulfill the entire industry demand at a price below costs. (x) the cost of predation should be less than the profits incurred through driving out one’s rivals from the

In order for a firm to profit from predatory pricing: (w) the incumbent must fulfill the entire industry demand at a price below costs. (x) the cost of predation should be less than the profits incurred through driving out one’s rivals from the

For a competitive firm the short-run supply curve is the: (w) marginal cost curve which is above the average total cost curve. (x) marginal cost curve which is above the average variable cost curve. (y) upward sloping part of the marginal cost curve.

The marginal utility most obviously diminished whenever: (1) Eric sang six songs rather than only one on karaoke night at local club. (2) Molly’s piano lessons absorbed 20 hrs last week she could have used up for studying. (3) Karen built 12 boxes however only 9

18,76,764

1958208 Asked

3,689

Active Tutors

1424007

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!