Portfolio return probability

XY Company has made a portfolio of such three securities: The correlation coefficient among Limpopo and Kasai is 0.6. When the returns are generally distributed, determine the probability that the return of portfolio is more than 15%.

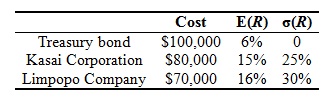

XY Company has made a portfolio of such three securities:

The correlation coefficient among Limpopo and Kasai is 0.6. When the returns are generally distributed, determine the probability that the return of portfolio is more than 15%.

PV of dividends: Cortez, Inc., is expecting to pay out a dividend of $2.50 next year. After that it expects its dividend to grow at 7 percent for the next four years. What is the present value of dividends over the next five-year period if the required rate of return is 10 percent?

When valuing the shares of my company, I calculate the present value of the expected cash flows to shareholders moreover I add to the result obtained cash holdings and liquid investment. Is that correct?

Why classical option pricing with constant volatility required?

Could we explain that goodwill is equal to brand value?

Which are the essential hypotheses so that valuations of the Economic Value Added (EVA) give similar results to discounting cash flows?

Who explained the high-peak/fat-tails?

Inventory is an important part of WCR estimation. It is a current asset, which depletes over period of time. Also, it requires creation of facility, which would help in storing the inventory and estimate the associated cost of maintaining and transporting it. The esti

Tudor Online Publishing Corporation has tax rate of 35%, debt-to-equity ratio of 25%, and has (leveraged) beta 1.25. The riskless rate is 3% and the market return is 12%. Windsor Publishing Company is an all equity company and is in the same business. What is the requ

Who were the creators of uncertain volatility model?

You expect KT industries (KTI) will have earnings per share of $3 this year and expect that they will pay out $1.50 of these earnings to shareholders in the form of a dividend. KTI's return on new investments is 15% and their equity cost of capital is 12%. The value of a share of KTI's stock is clos

18,76,764

1931544 Asked

3,689

Active Tutors

1434580

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!