Perfectly price inelastic demand

For Cournot’s Spring Water the demand is perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c (iv) point d. (v) point e. Hey friends please give your opinion for the problem of Economics that is given above.

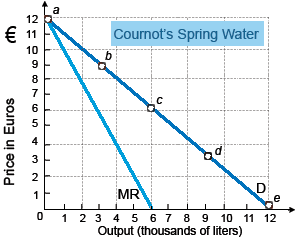

For Cournot’s Spring Water the demand is perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c (iv) point d. (v) point e.

Hey friends please give your opinion for the problem of Economics that is given above.

If the government puts a rent ceiling of $650 a month, what is the rent paid and how many rooms are rented? Explain why?

Maintenance of monopoly power is improved by: (1) natural barriers to entry. (2) large economies of scale. (3) artificial barriers. (4) legal barriers to entry. (5) All of the above. Hello guys I want your advice.

Short-run market supply curve of a competitive industry is derived by summing all the firms’: (1) average cost curves vertically. (2) short-run supply curves horizontally. (3) production capacities along with the resources available. (4) individ

An unregulated monopoly is a market structure: (w) which is especially inefficient when price discrimination is practiced. (x) inhabited by several firms, all selling identical goods. (y) composed of a single firm which controls the production and pri

I have a problem in economics on Jollies gained-Production occurs. Please help me in the following question. The jollies gained whenever production takes place do not comprise utilities of: (i) Form. (ii) Possession. (iii) Place. (iv) Substance. (v) T

I have a problem in economics on Short run for production. Please help me in the following question. In short run for production: (1) Both variable and fixed costs exist. (2) Productive capacity might be adjusted. (3) Unprofitable firms shut down. (4) No fresh workers

Contestable markets and purely competitive markets share the feature of: (w) collusive behavior of huge firms. (x) freedom of entry and exit into the long run. (y) widespread product differentiation. (z) persistent economic profits. Q : Arc elasticity formula for price When raising subscription rates to the News and Observer from $8 to $10 monthly cause newspaper sales to drop by 180,000 to 120,000 copies daily, using the arc elasticity formula, then price elasticity of demand equals to: (1) 0.9. (2

When raising subscription rates to the News and Observer from $8 to $10 monthly cause newspaper sales to drop by 180,000 to 120,000 copies daily, using the arc elasticity formula, then price elasticity of demand equals to: (1) 0.9. (2

The percentage of a specific population who is either unemployed or employed or is termed as the: (i) Labor force participation rate. (ii) Work-force proportion. (iii) Income-leisure loss curve. (iv) Substitution effect dominance rate. (v) Labor supply.

This would be most complicated for resource owners to forward-shift a tax onto: (w) capital. (x) accounting profit. (y) land. (z) labor. Can someone explain/help me with best solution about problem of Econo

18,76,764

1941861 Asked

3,689

Active Tutors

1457586

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!