Perfectly price elasticity of supply

The supply of textile employees in China is possibly most like the perfectly price elastic supply curve within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. How can I solve my Economics problem? Please suggest me the correct answer.

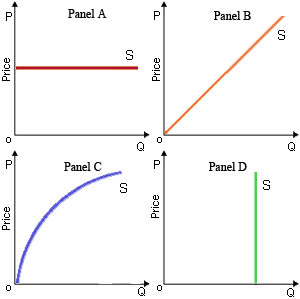

The supply of textile employees in China is possibly most like the perfectly price elastic supply curve within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

How can I solve my Economics problem? Please suggest me the correct answer.

The phrase ‘dollar votes’ refers to the consumers: (1) Voting patterns in the national elections. (2) Recognizing what goods are produced. (3) Each containing an equivalent says about what is generated. (4) Being subservient to big firms. Q : Problem on market demand for housing All as well equivalent, population growth would tend to rise the: (i) Demand for housing for each and every family. (ii) Supply of natural resources. (iii) Shares of family budgets spend on luxuries. (iv) Market demand for housing.

All as well equivalent, population growth would tend to rise the: (i) Demand for housing for each and every family. (ii) Supply of natural resources. (iii) Shares of family budgets spend on luxuries. (iv) Market demand for housing.

Illustrations of pairs of goods which are close substitutes comprise: (i) Bow ties and tuxedoes. (ii) Glasses and contact lenses. (iii) Power boats and water skis. (iv) Baby food and diapers. (v) Camping trailers and large SUVs. Q : Production and costs in monopolistic In the short run, no profit-oriented monopolistically-competitive firm still knowingly generates any output unless: (1) an economic profit is assured. (2) total revenues are expected to equal or exceed its total variable costs. (3) the average wage ra

In the short run, no profit-oriented monopolistically-competitive firm still knowingly generates any output unless: (1) an economic profit is assured. (2) total revenues are expected to equal or exceed its total variable costs. (3) the average wage ra

The two policies that most likely account for most of the trend toward greater income equality during 1929 and 1975 are: (w) improved educational opportunities, and tax and transfer policies. (x) reduced sex discrimination and public availability of b

Normal 0

A firm which realizes an economic profit in the short run will carry on generating economic profits in the long run only when: (i) it maximizes economic revenue. (ii) barriers to entry prevent entry from rival firms. (iii) its managers minimize princi

The present value of an annual income stream which goes on forever equals the annual income as: (w) times infinity. (x) divided by the wage rate. (y) multiplied by the interest rate. (z) divided by the interest rate. Q : Marginal cost curve in market power Above the minimum average variable cost curve, the marginal cost curve is not the supply curve of a monopoly since, unlike purely competitive firms, firms along with market power: (w)

Above the minimum average variable cost curve, the marginal cost curve is not the supply curve of a monopoly since, unlike purely competitive firms, firms along with market power: (w)

I have a problem in economics on Buyer beware-Laws and Regulations. Please help me in the following question. Caveat emptor signifies: (i) Let the sellers beware. (ii) Sellers are the most excellent judges of the quality of their goods. (iii) Charge w

18,76,764

1951984 Asked

3,689

Active Tutors

1454935

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!