Perfectly inelastic supply of labor

Glynn’s supply of labor is perfectly inelastic at: (1) point a. (2) point b. (3) point c. (4) point d. (5) point e. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

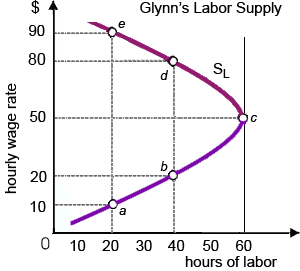

Glynn’s supply of labor is perfectly inelastic at: (1) point a. (2) point b. (3) point c. (4) point d. (5) point e.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

The marginal utility [that is, additional jollies derived from the final unit consumed] of each and every of the specific goods you purchase regularly is probably most intimately correlated with each and every good’s: (1) Consumer surplus. (2) Market price. (3)

Interest rates on specified financial instruments tend to be lower the: (1) shorter the period to maturity. (2) greater the risk of default. (3) less liquid is the asset. (4) greater the expected rate of inflation. (5) greater the face value is relati

When pharmaceutical manufacturers conspire to generate only Q1 penicillin, in that case the: (i) purely-competitive firms which produced penicillin would experience economic losses. (ii) resulting excessive antibiotic treatments would produce strains of dru

Expectations of long-run economic losses within a competitive industry as: (1) inevitably follow “cut throat” pricing policies. (2) cause firms to leave the industry. (3) increase each firm’s long-run fixed costs. (4) create pressure

Monopolistic competitors: (1) base decisions on the anticipated reactions of their many individual competitors. (2) can easily enter but not exit industries. (3) may sometimes act like monopolists and gain economic profits in the short run because of

Within this "kinked-demand curve" model, that firm views the demand curve this faces as the: (w) linear "kinked" demand curve aD2 for all prices. (x) linear "kinked" demand curve D1D1 for all prices. (y) nonlinear "kin

Even when each household’s demand curve didn’t shift, the market demand for the butter would increase if there were a raise in: (1) House-hold income. (2) People’s preferences for the butter. (3) Population. (4) Price of margarine.

Several buyers and sellers are forced to be price-takers since: (w) vigorous competition maintains individuals from noticeably influencing the market. (x) only monopoly firms adjust quantities. (y) markets adjust slowly. (z) quantity adjustment is not

Illustrations of transfer programs do not comprises: (w) welfare payments. (x) food stamps. (y) aid for dependent children (AFDC). (z) corporate income taxes. Hello guys I want your advice. Please recommend some vi

A kinked demand curve for an oligopoly is probably when: (1) all the rival firms face identical demand curves. (2) rival firms are expected to match price cuts, but not price hikes. (3) firms ignore their rivals’ strategies when

18,76,764

1951671 Asked

3,689

Active Tutors

1423178

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!