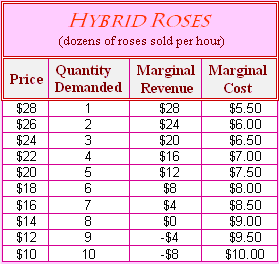

Hybrid Roses is the merely florist in 60 miles of Presidio, Texas. When total fixed costs (for example, rent and utilities) are $9 per hour, such profit-maximizing monopolist will generate an output of: (1) two dozen roses per hour. (2) four dozen roses per hour. (3) six dozen roses per hour. (4) eight dozen roses per hour. (5) ten dozen roses per hour.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?