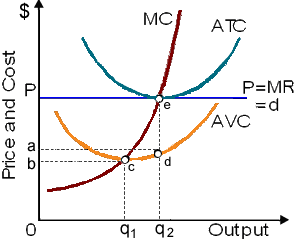

Output level on marginal revenue and marginal cost

When the firm produced at output level q2, this produced where: (w) MR = MC. (x) MR > MC. (y) MR < MC. (z) P < MC. Can someone explain/help me with best solution about problem of Economics...

When the firm produced at output level q2, this produced where: (w) MR = MC. (x) MR > MC. (y) MR < MC. (z) P < MC.

Can someone explain/help me with best solution about problem of Economics...

The total revenue of a firm which faces a negatively-sloped demand curve: (w) is at a maximum where marginal revenue is zero. (x) declines while average revenue falls as output grows. (y) rises at an increasing rate over the output range plagued throu

Name the System of Note-issue in India. Answer: In India, the system of note-issue is the Minimum Reserve System. The RBI is needed to keep minimum reserves of Rs 2

In the year 1960s, suburbanites start to landscape by employing bark which had formerly been discarded whenever Clear-Cut Forestry Products turned logs to lumber whereas decimating old-growth forests. The extra operating revenue to Clear-Cut from selling bags of bark

After the minimal materials essential for survival are attained, poverty becomes: (w) an absolute concept. (x) more prevalent in North America than elsewhere. (y) measured by the income level required to meet minimal psychological needs. (z) a relativ

Can someone help me in finding out the right answer from the given options. The substitute goods are: (i) Usually consumed altogether. (ii) Inferior to luxury goods. (iii) Generally free goods. (iv) Replacements for each other. Q : Marginal revenue and monopoly For a For a nondiscriminating monopolist, the marginal revenue is: (w) identical to price. (x) always positive. (y) always less than price. (z) always greater than price. Hello guys I want your advice. P

For a nondiscriminating monopolist, the marginal revenue is: (w) identical to price. (x) always positive. (y) always less than price. (z) always greater than price. Hello guys I want your advice. P

A perpetuity currently priced at $5000 which will pay $200 annually all times generates a rate of return of: (w) 4%. (x) 4.8%. (y) 5%. (z) 3.5%. Hey friends please give your opinion for the problem

Marginal revenue is not below the market price by the perspectives of simply: (i) monopolistic competitors. (ii) monopolists. (iii) cartel members. (iv) pure oligopolists. (v) pure competitors. Can

When Nostalgia Corporation maximizes profit in its production of Silver Screen DVDs, in that case its annual total costs will be around: (i) $45 million. (ii) $65 million. (iii) $85 million. (iv) $105 million. (v) $125 million. <

Assume a neither firm possessing both the monopsony power as an employer and the market power in its output market, however which can neither wage discriminate nor price discriminate. In the equilibrium in its labor market for workers, of the given va

18,76,764

1931021 Asked

3,689

Active Tutors

1423432

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!