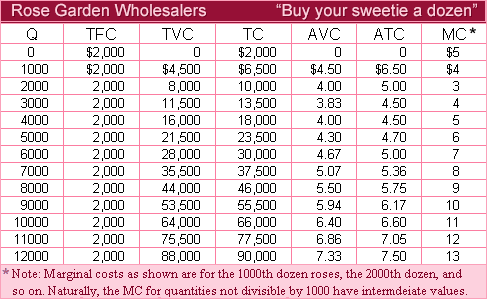

When the wholesale price per dozen roses is $4.50, the breakeven point for Rose Garden Wholesalers happens at an output level of about: (i) 2000 dozen roses. (ii) 2500 dozen roses. (iii) 3000 dozen roses. (iv) 3500 dozen roses. (v) 4000 dozen roses.

Hello guys I want your advice. Please recommend some views for above Economics problems.