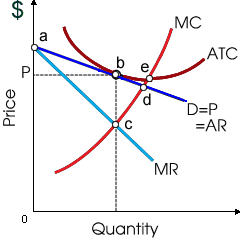

This monopolistic competitor generates Q0 output and experiences: (1) only normal accounting profits, and zero economic profits. (2) positive economic profits. (3) high costs because of excessive managerial salaries. (4) stagnation because of brand name deterioration. (5) economic losses.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.