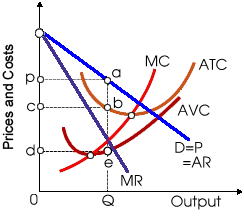

This monopoly makes Q units and experiences as: (1) economic profits equal to 0cbQ. (2) economic losses equal to cpab. (3) more than normal accounting profits. (4) marginal cost in excess of average total cost. (5) total revenue less than total cost.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?