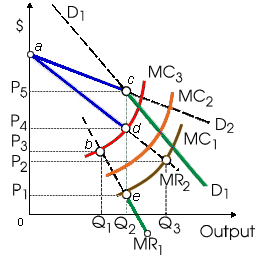

Within this "kinked-demand curve" model, that firm views the demand curve this faces as the: (w) linear "kinked" demand curve aD2 for all prices. (x) linear "kinked" demand curve D1D1 for all prices. (y) nonlinear "kinked" demand curve D1cD2. (z) nonlinear "kinked" demand curve acD1.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.