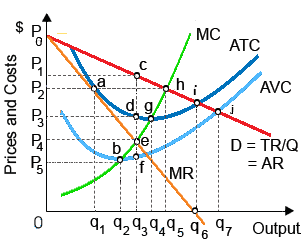

HoloIMAGine has patented a holographic technology which creates 3-D photography obtainable to consumers. There is a market supply curve for HoloIMAGine technology: (w) nonexistent since price-maker firms simultaneously set prices as well as quantities depend on the structures of market demands and their own costs. (x) perfectly price elastic at a price of P1. (y) equal to the marginal cost [MC] curve above point b. (z) perfectly price inelastic at quantity q3.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?