Most perfectly price inelasticity in supply curve

In illustrated graph below, supply is mostly perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c. (iv) point d. Hey friends please give your opinion for the problem of Economics that is given above.

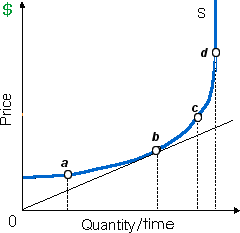

In illustrated graph below, supply is mostly perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c. (iv) point d.

Hey friends please give your opinion for the problem of Economics that is given above.

Curing scarcities in the market for ice cream needs: (i) Rises in the price of ice cream. (ii) Reduces in the supply of ice cream. (iii) Rises in the demand for ice cream. (iv) Reduction in the price of ice cream. (v) Burden of a price floor.

Economic discrimination occurs while: (1) economic rents are received by resource suppliers. (2) wages are proportional to workers’ differing productive contributions. (3) household incomes differ because of different resource ownership. (4) pur

Can someone help me in finding out the precise answer from the given options that when a fixed level of national income becomes appreciably less evenly distributed as the numbers of relatively poor people and relatively prosperous people both raise dr

Expansion of the industry in increasing cost industries causes: (w) increases in each firm’s costs at every level of output. (x) decreases in each firm’s costs at every level of output. (y) all firms to suffer long-run economic losses. (z)

Can someone help me in finding out the precise answer from the given options. The citizens in lower 48 states utilize lots of wild Alaskan salmon till a major oil spill close to Anchorage spoils the fishing. The ____ of salmon will increase whereas the ____ reduces. (

Jay saved $200 to purchase a Zowie digital camera following her friend showed Jay the Zowie she purchased for $200 at a close by camera store. Fortunately the camera was on sale for $150 all through a one-hour ‘Manager’s Special’ sale when Jay ultima

State excess demand or inflationary gap: Excess demand takes place whenever AD is bigger than AS at the level of full employment equilibrium.

Programs which guarantee farmers minimum prices which exceed equilibrium prices will yield: (w) cheaper food for consumers. (x) excess demand in food markets. (y) excess supply at the minimum price. (z) higher equilibrium prices.

In the quintile distribution of income, the term "quintile" represents

For such illustrated figure profit-maximizing pure competitor, there area aPed shows: (1) fixed cost (TFC). (2) average fixed cost (AFC). (3) the lowest possible economic loss. (4) maximum economic profits. (5) the rate of return on investment. <

18,76,764

1938611 Asked

3,689

Active Tutors

1458863

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!