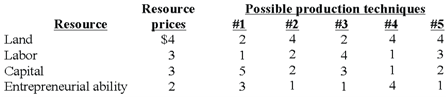

Refer to the given data give the answer of following question. In view of the indicated resource prices, the economically most efficient production technique(s) is (are) technique(s): A) #1. B) #2 and #4. C) #3. D) #1 and #3.

Help me to get through this problem