Monopolistic competitor in market

When this monopolistic competitor makes Q units: (1) P > MC. (2) MR = MC. (3) total revenue total cost is maximized. (4) MSB > MSC. (5) All of the above. Please guys help to solve this problem of Economics with some explanation.

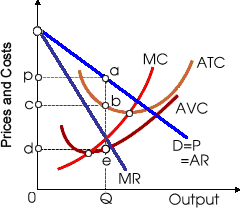

When this monopolistic competitor makes Q units: (1) P > MC. (2) MR = MC. (3) total revenue total cost is maximized. (4) MSB > MSC. (5) All of the above.

Please guys help to solve this problem of Economics with some explanation.

I have a problem in economics on Demand Curve when price is cut. Please help me in the following question. When the price of Snapple is cut, then: (1) The lower quantity of Snapple is demanded. (2) A bigger quantity of Snapple is demanded. (3) Demand for the Snapple r

A straight-line that positively sloped supply curve which starts from the basis is: (w) elastic for all prices and quantities. (x) inelastic for all prices and quantities. (y) unitarily elastic for all quantities and prices. (z) negatively associated

When all bonds are perpetuities which pay annual income of $50, at an interest rate of 5% the price of bonds is: (w) $1,000. (x) $500. (y) $100. (z) $750. Can someone explain/help

Total revenue equals: (w) price times quantity. (x) marginal revenue times marginal cost. (y) profit per unit of output. (z) total cost minus profit. Please choose the right answer from above...I want your suggesti

Objectives: This assessment item relates to the course learning outcomes 1, 2 and 3 as listed in Part A. Question 1 (22 marks) (a) Consider the market represented by the schedule in the table below. (5 marks) Price Quantity demanded Quantity

Describe what do you mean by the term Yield to Maturity?

Tell me the answer of this question. Critics of the North American Free Trade Agreement (NAFTA) falsely feared that it would: A) increase the flow of illegal Mexican immigrants to the United States. B) cause the European Union and Japan to raise trade barriers against

When the import market was within equilibrium before the Japanese government began subsidizing all autos exported by the amount dg, in that case U.S. car buyers would be: (w) pay P2 for a car previouslszy priced at P0. (x) suffer Q0 to

Under the negative income tax system demonstrated in this figure, where a family of four all along with earned income of $60,000 yearly would have a net [after-tax] income of: (1) $37,500 per year. (2) $42,500 per year. (3) $50,000 per year. (4) $55,0

St. Valentine’s Day software is currently going in version of 6.0. At this point on the demand curve where the price elasticity of demand is unitary, there the price would be approximately: (i) $20, resulting in roughly 16 milli

18,76,764

1935535 Asked

3,689

Active Tutors

1415460

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!