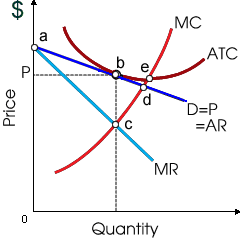

This figure demonstrates a: (w) long run equilibrium for a firm in a perfectly competitive industry. (x) short run equilibrium for a natural monopoly. (y) short run circumstances for a monopolistically-competitive firm into long run equilibrium. (z) cartel which maximizes joint-monopoly profits for the oligopolists which are members.

Hey friends please give your opinion for the problem of Economics that is given above.