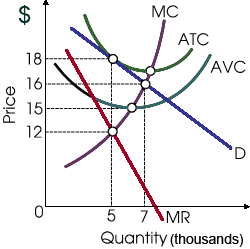

When this firm initially had important market power along with potential long-run economic profit, a likely cause of the firm finally being in a stable equilibrium of an $18 price and output of 5,000 units every day would be: (1) successful efforts by its workers to organize an aggressively militant union. (2) entry by numerous foreign firms in order that this market became monopolistically competitive. (3) successful antitrust action by the Federal Trade Commission. (4) acquisition by a firm not plagued by managerial slack.

How can I solve my Economics problem? Please suggest me the correct answer.