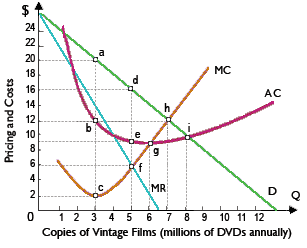

Nostalgia Corporation could accomplish minimum average costs for Silver Screen DVDs when this produced: (i) 4 million DVDs. (ii) 6 million DVDs. (iii) 8 million DVDs. (iv) 10 million DVDs. (v) 12 million DVDs.

Hey friends please give your opinion for the problem of Economics that is given above.