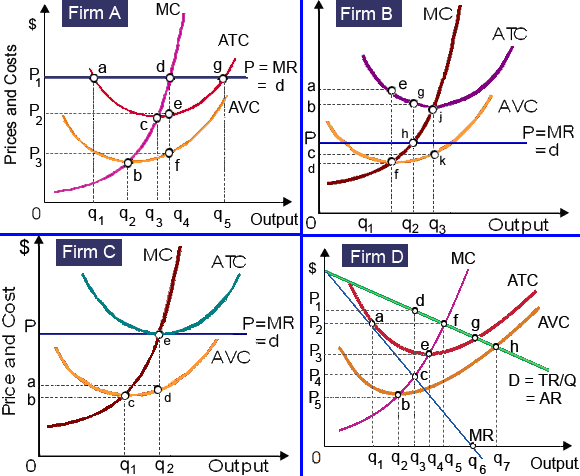

When Firm B in demonstrated graph successfully minimizes losses and maximizes its profits that have: (1) covered overhead while incurring short-run economic losses. (2) potential economic profit of Pbgh per period. (3) total costs equal to 0phq2. (4) produced the socially optimal rate of output for the entire market. (5) covered its variable costs but is incurring short-run economic losses.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.