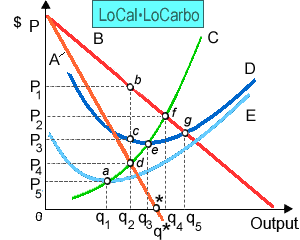

LoCalLoCarbo that is Favorite Corporation of fad dieters, which can minimize its average total costs near producing: (i) output q1 at point a. (ii) output q2 at point b. (iii) output q3 at point e. (iv) output q4 at point f. (v) output q5 at point g.

Can someone explain/help me with best solution about problem of Economics...