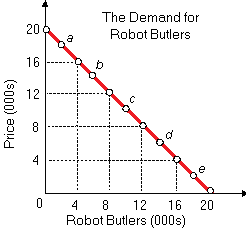

The elasticity of demand equals one and consumer spending upon Robot Butlers (there is the firm’s total revenue), is at a maximum at a price of as: (1) $20,000. (2) $15,000. (3) $10,000. (4) $5,000. (5) zero.

Please choose the right answer from above...I want your suggestion for the same.