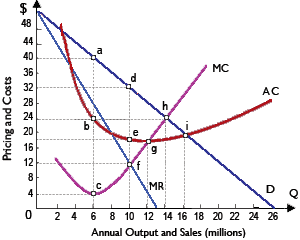

Maximum possible total revenue by sales of the especially popular St. Valentine’s Day software is about: (i) $140 million. (ii) $250 million. (iii) $350 million. (iv) $420 million. (v) $1 billion.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.