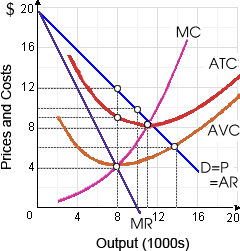

This firm’s maximum possible economic profit equals: (i) $12,000 per period. (ii) $16,000 per period. (iii) $20,000 per period. (iv) $24,000 per period. (v) $28,000 per period.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?