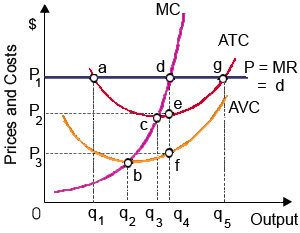

When this competitive firm operates at point d in demonstrated graph, in that case this: (w) could increase profits by expanding output to q5. (x) maximizes economic profit [ as area P2P1de], but these profits will evaporate in the long run as new firms enter the industry. (y) minimizes economic losses, that equal area P3P2ef. (z) experiences total fixed costs equal to area OP1dq4.

Can someone explain/help me with best solution about problem of Economics...