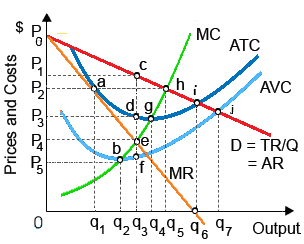

HoloIMAGine has patented a holographic technology which creates 3-D photography obtainable to consumers. It maximizes profit at: (i) output q1. (ii) output q2. (iii) output q3. (iv) output q4. (v) output q5.

How can I solve my Economics problem? Please suggest me the correct answer.