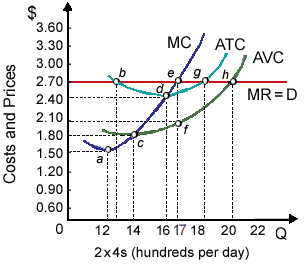

Profit is maximized as in illustrated graph when this purely-competitive lumber mill produces at: (1) point a. (2) point b. (3) point c. (4) point d. (5) point e.

Hello guys I want your advice. Please recommend some views for above Economics problems.