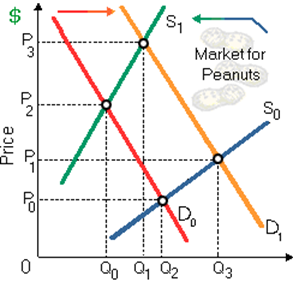

Specified the shifts demonstrated in the market for peanuts, there is the: (1) price will fall.(2) quantity of output will rise slightly. (3) supply has fallen while demand has grown. (4) main adjustment happens in the quantity exchanged. (5) vast shortage was cured by increasing supply and slack demand.

Please choose the right answer from above...I want your suggestion for the same.