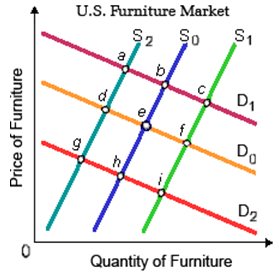

When market begins in equilibrium at point e upon S0D0 and in that case young American families increasingly "inherit" furniture like their baby-boomer parents move within smaller retirement homes, that market will tend to shift in the direction of: (1) point i. (2) point h. (3) point a. (4) point d. (5) point f.

How can I solve my economics problem? Please suggest me the correct answer.