Market power as a price maker

The only firm in this figure which has market power as a price maker is: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D. I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.

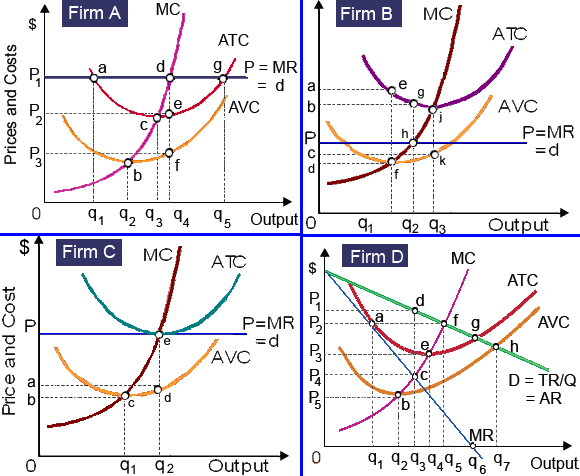

The only firm in this figure which has market power as a price maker is: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.

I have a problem in economics on Equilibrium rate of monopsony exploitation. Please help me in the following question. Equilibrium rate of the monopsony exploitation by a firm is a difference between: (i) MRP and VMP. (ii) VMP and w. (iii) MFC and w.

Why does a marginal benefit curve slope downwards?

In the above diagram, the elimination of discrimination is best represented by:

I have a problem in economics on Examples of perishable goods. Please help me in the following question. Illustrations of perishable goods comprise: (1) The book Carrie reads each and every night before brushing her teeth. (2) The computer Barry emplo

Can someone please help me in finding out the accurate answer from the following question. The synonymous words of marginal factor costs or marginal resource costs signify to the: (i) Cost incurred in generating an extra unit of capital. (ii) Cost to the resource owne

This binge drinking exercise observes why excessive drinking might be an economic trouble and the possible influences of government policy.

‘Describe the influence of London Olympics on economy?’

When a monopolist produces output where demand is unitarily elastic, in that case marginal revenue equals: (1) price. (2) infinity. (3) negative infinity. (4) one. (5) zero. I need a good answer on the topic of

Can someone help me in finding out the precise answer from the given options. Modifying the goods or resources in manners that make them more valuable is: (1) Production. (2) Profitability. (3) Consumption. (4) Distribution.

The economy consists of two consumers, A and B. Both consumers are endowed with one unit of good 1 and one unit of good 2. Consumer A is entirely indifferent between all consumption plans. Consumer B has the utility function u(xB1 ; xB

18,76,764

1946574 Asked

3,689

Active Tutors

1420310

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!