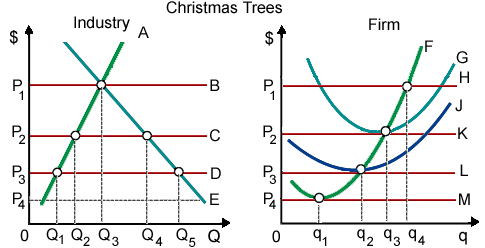

At the price P1, this purely competitive Christmas tree industry is within: (w) long-run equilibrium. (x) short-run equilibrium. (y) market period disequilibrium. (z) short-run disequilibrium.

Hello guys I want your advice. Please recommend some views for above Economics problems.