Market initially at price and quantity

This market for peanuts is primarily into equilibrium at price: (w) P0 and quantity Q0 (x) P1 and quantity Q0 (y) P2 and quantity Q2 (z) P1 and quantity Q1 How can I solve my economics problem? Please suggest me the correct answer.

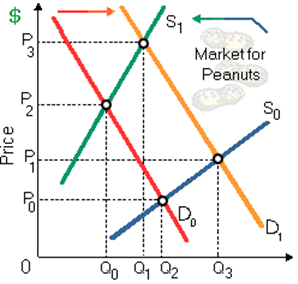

This market for peanuts is primarily into equilibrium at price: (w) P0 and quantity Q0 (x) P1 and quantity Q0 (y) P2 and quantity Q2 (z) P1 and quantity Q1

How can I solve my economics problem? Please suggest me the correct answer.

When a change in the supply of a good causes a percentage change within price which exceeds in absolute value the resulting percentage change within quantity demanded, then demand is relatively: (1) price elastic. (2) inferior. (3) no

The Overpriced Petroleum Extraction Company (or OPEC) has just declared its acquisition of some small firms with facilities which will permit OPEC to process oil via the whole refining procedure, from oil field recovery via transporting and then trading the refined pe

Whenever a tax on a good outcome less government revenue than the sum of the losses of producer and consumer surpluses due to tax, economists state that the tax has caused a/an: (1) Administrative loss. (2) Market failure. (3) Economic loss. (4) Bureaucratic loss. (5)

Refer to the given figure.Choose the right answer from following. If the relevant saving schedule were constructed: A) saving would be minus $20 billion at the zero level of income. B) aggregate saving would be $60 at the $60 billion level of income. C) its slope woul

The demand for durable consumer good tends to rise if: (1) Supply rises. (2) Aggregate expenses rise. (3) Consumers predict price hikes or scarcities in the future. (3) Consumers predict surpluses in future. Choose the precise answ

Total revenue roughly for the profit-maximizing lumber mill equivalents: (i) $1700 daily. (ii) $2500 daily. (iii) $3500 daily. (iv) $4590 daily. (v) $6000 daily. Q : Screening and Credentialism The critics The critics of ‘credentialism’ suppose that firms making employment decisions tend to mainly rely too heavily on: (i) Personal contacts. (ii) Personality testing. (iii) Past experience. (iv) Job interviews. (v) Formal education and trainin

The critics of ‘credentialism’ suppose that firms making employment decisions tend to mainly rely too heavily on: (i) Personal contacts. (ii) Personality testing. (iii) Past experience. (iv) Job interviews. (v) Formal education and trainin

Can the value of APS be negative:Yes, the value of APS is negative; when there are dissavings.

When drought causes ranchers to in advance take cattle to the market, one short-run tendency will be for: (1) The demand for beef to rise. (2) Restaurants to experience shortages of the steak. (3) Prices for pork and lamb to decline. (4) Corn and wheat to become less

An imperfectly competitive firm can maximize profit within the long run only at prices and also outputs where demand elasticity is: (w) greater than or equal to 1. (x) less than 1. (y) less than 0. (z) between 0 and 1. Discover Q & A Leading Solution Library Avail More Than 1416083 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1928591 Asked 3,689 Active Tutors 1416083 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1928591 Asked

3,689

Active Tutors

1416083

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!