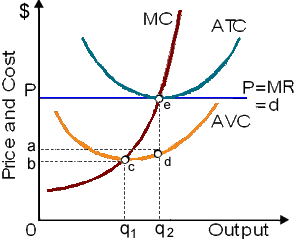

Ceteris paribus, inside the short run an increase into the market demand for this product would permit this purely competitive firm to be: (w) make only normal profits. (x) break even. (y) make economic profits, although not in the long run. (z) compete.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.