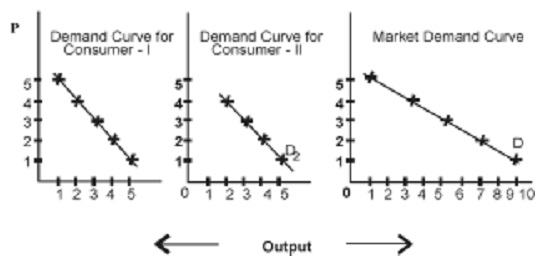

Market demand curve:

The market demand also rises with a fall in price and vice-versa.

In figure below the quantity demanded by consumer I and consumer II are measured on horizontal axis and the market price is computed on the vertical axis. The net demand of these two consumers that is, D1 + D2 = DDM - DDM – the market demand curve - as well slopes downwards just similar to the individual demand curve. Similar to normal demand curve, it is convex to the origin. It reveals the inverse relationship.