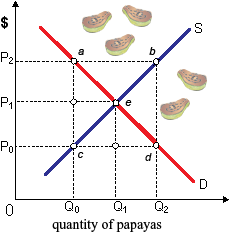

Within below figure there is market for papayas: (1) a shortage exists at P2. (2) papayas are a free good at P0. (3) papayas are currently a scarce good. (4) consumer's demand prices equivalent P2 at quantity Q2. (5) the equilibrium price for papayas is P0.

How can I solve my economics problem? Please suggest me the correct answer.