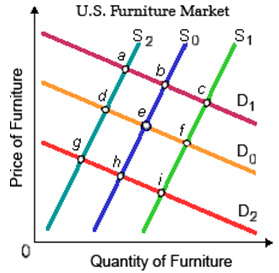

When the U.S. furniture market is primarily in equilibrium at point e upon S0D0 and in that case Chinese manufacturers begin exporting more furniture to the United States, that market would move in the direction of a new equilibrium at: (1) point a. (2) point b. (3) point c. (4) point d. (5) point f.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?